By: Ankit Sood

Key takeaways

- Tailored Approach to Insurance Procurement: Insurance procurement requires a specialized approach due to the unique nature of the industry, focusing on risk management, cost containment, and customer experience enhancement.

- Role of Data Analytics and AI: Data analytics and AI play a crucial role in navigating market trends, optimizing operational models, and enhancing decision-making processes in insurance procurement.

- Comprehensive Solutions from SpendEdge: SpendEdge offers tailored solutions for insurance procurement, empowering companies to mitigate risks, reduce costs, and improve operational efficiency through supply-side risk management and optimized negotiations.

- Maximizing Value Delivery: By optimizing claims management, enhancing supplier contracts, and leveraging market intelligence, SpendEdge enables insurance organizations to thrive in a competitive landscape and maximize value delivery.

The peculiar nature of insurance business, which is essentially based on the spreading of risks evenly across a large number of contributors or broader population, makes procurement in the sector unlike any other. Another atypical feature of the sector is that insurers prefer to sell products to even large corporate customers via brokers. By contrast, banking customers can buy products directly from a bank or from a broker. Setting aside a certain amount as “reserve funding,” including to meet the cost of claims that might arise in the future, is a legal obligation for insurers. Too high a reserve might increase the cost of insurance cover for customers. On the other hand, if reserves are too low, there is a risk that the insurer might run out of the funds needed to meet future claims! In sum, procurement in insurance is at variance with what’s practiced in other industries. The steps and actions in insurance procurement would include framing accurate risk profiles of clients, improving risk coverage while optimizing premiums, delivering high-touch customer experiences, stripping out unnecessary costs and inefficient processes, and emphasizing the role of the insurance broker as a viable intermediary.

Importance of insurance procurement for value delivery

Putting a number to the level of uncertainty a business is willing to endure

Evaluating the risks in the way of doing business and inventorying them on the “most important to least important” scale marks the beginning of the journey in insurance procurement for any enterprise. It is very unlikely for any two businesses to have the exact same risk profile, and this tends to vary across functions and facets like operations, finance, legal compliance, workplace health and safety, and organizational reputation. A company with operations outside its home country will likely be exposed to financial risks resulting from exchange rate fluctuations and is better served by foreign exchange insurance. Therefore, identifying and getting a true measure of the risks hovering over a business is key to making informed decisions around business insurance procurement. Insurance analytics and AI come to the rescue here.

Creating the right financial safety net for the organization

The type of risk coverage a business typically considers and the insurer it chooses to go with are premised on its risk profile. For instance, there are different kinds of marine risk cover; some provide no more than supplementary protection (e.g., carrier legal liability insurance) while others (e.g., all-risks cargo insurance policy) offer much broader coverage against damage or loss occurring to cargo in transit. So, failing to choose the right risk cover or top-up insurance for additional coverage might deprive cargo shippers of financial protection for the actual value of the goods shipped. Moreover, businesses look for multiple risk coverages to secure themselves against loss or damage suffered by their assets (e.g., property insurance) or against liability arising from the loss or damage their actions cause to others (e.g., casualty coverage). This can be a real challenge in insurance procurement services.

Coping with the cost of insurance crisis

The rising cost of commercial insurance cover is causing some consternation among customers. As in late 2022, the insurance industry was coughing up $100.70 in claims for every $100 of premium income! A number of factors have conspired to push up the price of insurance cover, key among them inflationary pressures, natural calamities, and business interruptions fueled by pandemics and geopolitical tensions. In 2023, umbrella coverage policies will likely cost a quarter more than the previous year while both property and auto insurance plans are going to be dearer by at least 9-10%. Amid rising hacking threats, cyber insurers are, on average, shelling out $60 in claims for every $100 of premium income. So, it should hardly be any surprise if cyber insurance premiums turn 75-100% costlier in 2023. Insurance actuarial services will probably have the final say.

Tackling the customer expectation gap in commercial insurance

In a dynamic world, CPOs need timely data on the status of their business’ insurance policy and gaps in commercial insurance coverage to enhance risk coverage without high premiums. Businesses often realize late in the day, much to their chagrin, that their vanilla insurance plan provides hardly any security against claims of sexual harassment and wrongful termination as well as business interruptions and cyberattacks. There could be major economic consequences. To keep such risks at bay and make more fact-based decisions, procurement teams might want insurers to provide them with accurate information on policy status, claim settlement, and level of risk coverage. However, commercial insurance is a sector that is struggling to close customer service gaps by their own admission! Not surprisingly, insurers’ capacity for high-touch customer experiences is becoming a key consideration in insurance procurement services.

Fashioning more efficient operating models

Insurers are trying hard to rein in runaway costs, which show little sign of easing. Multiple factors are working in tandem to jack up the cost structure, albeit to differing degrees, at insurance businesses. Insurers with an assortment of products and product lines are likely to have a higher percentage of sales costs than peers that carry limited products or single insurance plans. A lot of insurers still run legacy and standalone IT systems, which don’t “talk” well enough to each other. Proliferation of duplicate IT systems and data, which slows down decision making, carries significant cost implications for insurers and insurance claim processing companies, and these pass on to the customer. A breakdown of key cost drivers will help CPOs discover the true cost of an insurance product and use it as a bargaining chip in negotiations.

Best insurance procurement practices

Develop an accurate risk profile for the business

There are a host of risks looming large over businesses, in general, ranging from fire, theft, intentional damage, and natural hazards to accidents, litigation, cyberattacks, and more. Enterprises or, as is more likely, insurance consultants working on their behalf, make use of insurance risk assessment tools to recognize and gauge the severity (low, medium, high) of each risk type. Some of these critical risks might have the most detrimental effect on the running of a business and its quantifiable assets, including reputation. So, enterprises buy insurance protection against potential loss, damage, liability, or uncertainty stemming from severe risks that are beyond human control. This is significant from the standpoint of insurance procurement services.

Choose insurance cover based on actual need

Property insurance, general liability insurance, vehicle insurance, worker’s compensation insurance, and product liability insurance are some of the common risk covers most businesses choose to buy, of course in varying amounts. Umbrella policies that bundle in, say, business property and business liability insurance, at a discounted price, are also very popular with businesses. While choosing coverage, it is important to avoid the extremes of over insurance, an obvious drain on the purse, as well as under insurance, which leaves the business at the mercy of various uncertainties. Add-on covers that provide enhanced protection from natural disasters, human-created disasters (e.g., terrorist attacks), data thefts, and lawsuits are also significant. Procurement in insurance is an expensive and risky proposition, so it pays to take help from the experts.

Employ subtle but effective tactics to lower business insurance premiums

Business insurance premiums are surging. That said, there are ways CPOs can lower the cost of their commercial insurance and save hard-earned dollars. Procurement teams must read through the fine print of the insurance plan, though it can be an exercise in drudgery a lot of times, to make sure the cover that is being extended is precisely what the business needs. Insurance policies might come with unnecessary loadings that don’t necessarily matter to the client, and these are things best avoided to lower the cost of insurance. The higher a policy’s deductibles, the lower the premium. That’s the general case, and therefore, businesses should consider higher deductibles. Besides lawyers, negotiation companies and insurance consultants can help CPOs work out better coverage and lower premiums. Procurement in insurance has indeed a proactive role to play.

Cherry-pick insurers with the most optimal customer experience metrics

A lot of insurers acknowledge they are under growing pressure to improve customer experience, and the emergence of a new class of more sophisticated insureds in the past decade with clearer understanding of their insurance needs is giving new impetus to insurers’ efforts to enhance service levels. Insurers, for their part, are taking cognizance of the writing on the wall. Take the case of a leader in motor and travel insurance. Realizing that nearly a third of its customers were miffed with manual claim processing services, the company switched to an AI-based evaluation of images of damaged assets uploaded by customers, thus shrinking claim processing costs by a third and claim settlement time by a twelfth! Therefore, CXOs should invariably plump for insurers who provide superior and hassle-free customer interactions and experiences, leveraging faster insurance analytics and AI based processes while retaining the empathetic human touch (“high touch”).

Build a better lean cost model

Amid growing competition from born-digital insurers (e.g., Aviva’s digital native arm Quotemehappy.com), many incumbents are hard at work stripping out costs that do not add value for customers, besides rejigging their erstwhile revenue models. Certain traditional insurers have sold off their run-off businesses, which have ceased selling new policies but are liable for insurance plans on their books, to more efficient insurers. In December 2022, Sompo International announced the sale of its runoff, Endurance at Lloyd’s, to RiverStone International. Insurers are also consolidating their back-office or migrating them to lower cost destinations to trim operating expenses. Straight-through processing (STP), based on electronic transfers, is cutting out up to 90% of manual intervention to quicken claim payouts while paring operating costs. Meanwhile, a host of “insurtechs” (e.g., Lemonade) strong on data analysis, IoT, and AI are disintermediating the insurance sales process to sell direct to customers via websites and mobile apps. Insurance claim processing companies are also some of biggest beneficiaries of AI and IOT.

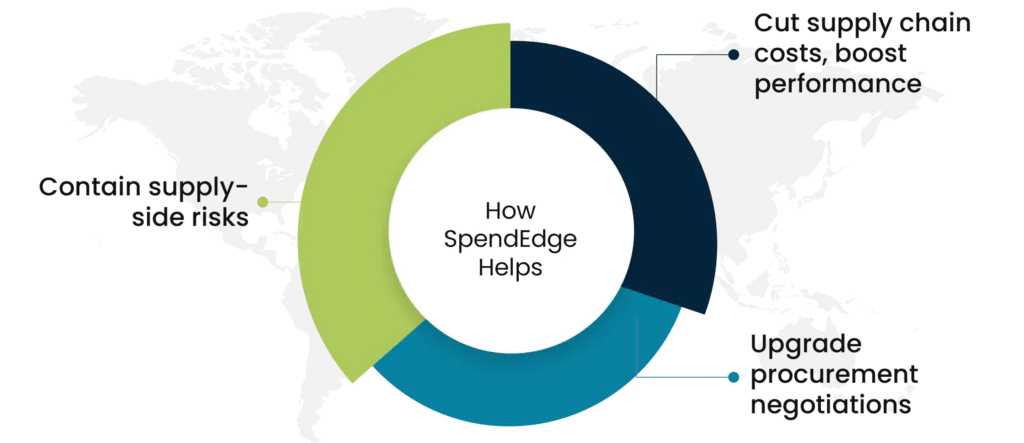

One stop solution – How SpendEdge can help transform insurance procurement with current trends

Contain supply-side risks

Our procurement specialists help insurers identify and brace themselves for a broad spectrum of risks. Furthermore, we help determine the likelihood of a potential risk occurring, its severity, impact on business growth and brand reputation. Insurance businesses typically face a variety of risks – financial, operational, strategic, as well as environmental, social, and governance. Our supply-side risk management framework for the insurance sector has all those previously mentioned bases covered. Most importantly, our experts are grounded in insurance analytics and AI, insurance actuarial services, as well as insurance procurement, including health insurance procurement.

Cut supply chain costs, boost performance

Clients in the insurance sector, including insurance claim processing companies, work closely with our insurance procurement specialists with significant experience to develop a better visibility of cost developments in the industry and discover ever-newer opportunities to better manage direct and indirect spend. Our deep and accurate insights into costs and benefits are enabling clients in the insurance sector to unlock new investment opportunities that deliver the most optimal ROIs.

Upgrade procurement negotiations

Negotiations with supply chain partners can be long-drawn-out and exhausting, and, at the end of it all, lead to poor outcomes, with insurance claim processing companies having to make too many concessions to pushy vendors. Our experts have up-to-the-minute data on supplier organizations, which our clients in the insurance domain can leverage as a negotiation-clinching chip to obtain better pricing and payment conditions. Moreover, by leaving the heavy lifting around the negotiation process to our experts, clients can focus on their core business, namely, providing financial protection to policyholders and generating appreciable surplus.

Success Stories: How SpendEdge helped insurance client mitigate risk with procurement intelligence

A North American property and casualty insurer with several millions in annual premium income was experiencing significant cost overruns. The company’s legacy IT system was the main culprit. The near-obsolete infrastructure and the poor quality of critical-to-business data in it were causing unintended loss of revenue for the client in the form of lost sales, customer turnover, and rising IT costs. Besides, insurers still running legacy platforms might soon be on the radar of insurance regulators, bringing with it the risk of hefty fines and reputational issues. Overall, poor line of sight into procurement spend data stood in the way of the client’s efforts to contain costs and improve margins. In June 2022, the client engaged our experts in insurance procurement to develop an actionable, analytics-driven solution to bolster insurance procurement services.

Our experts helped the client unlock opportunities for cost savings and containment, most of all, in back-office operations. Our recommendations included centralizing disjointed back-office tasks and shipping certain of them to more cost-efficient destinations. With a view to accelerating the sharing of transactional data from multiple sources across the enterprise and shrink payment cycle times, our experts recommended significant automation of procurement activities. This has also eliminated paper-based processes, manual data entry, and associated overheads in no small way. Our advisory has not only simplified the purchase process but also delayed the procurement organization to improve communication, visibility, and operational flexibility.

Our procurement solutions strictly tailored to the hitherto unmet needs of the insurance sector will drive down compliance costs and drive digital enablement. For more on this, contact us now.

Conclusion

The insurance sector’s unique characteristics demand a tailored approach to procurement. With a focus on risk management, cost containment, and customer experience enhancement, insurance procurement stands apart from other industries. Strategies involve creating accurate risk profiles, selecting appropriate coverage, and negotiating cost-effective contracts. Data analytics and AI play a crucial role in navigating market trends and customer expectations, while optimizing operational models helps in cost reduction and performance enhancement. SpendEdge offers comprehensive solutions for insurance procurement, empowering companies to mitigate risks, reduce costs, and improve operational efficiency. From supply-side risk management to upgrading procurement negotiations, our expertise drives tangible results. Our success stories underscore the value of our tailored approach in transforming insurance procurement and maximizing value delivery for insurance companies.

Author’s Details

Ankit Sood

Vice President, Sourcing and Procurement Intelligence

Ankit is working as a procurement specialist at Infiniti Research and has vast experience in leading market and procurement intelligence request for clients ranging across industries such as BFSI, CPG, F&B, Chemicals, and Pharmaceutical. He helps clients in solving procurement challenges related to supplier and competitive intelligence, cost optimization strategies, and overall market understanding.