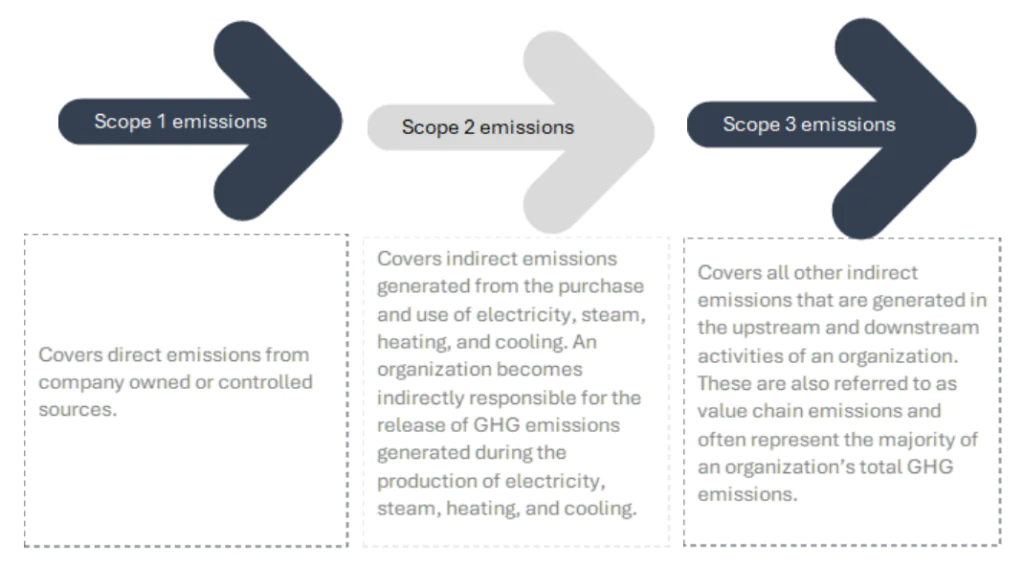

The Greenhouse Gas (GHG) Protocol provides the most widely recognised accounting standards for greenhouse gas emissions and categorizes GHG emissions into three Scopes.

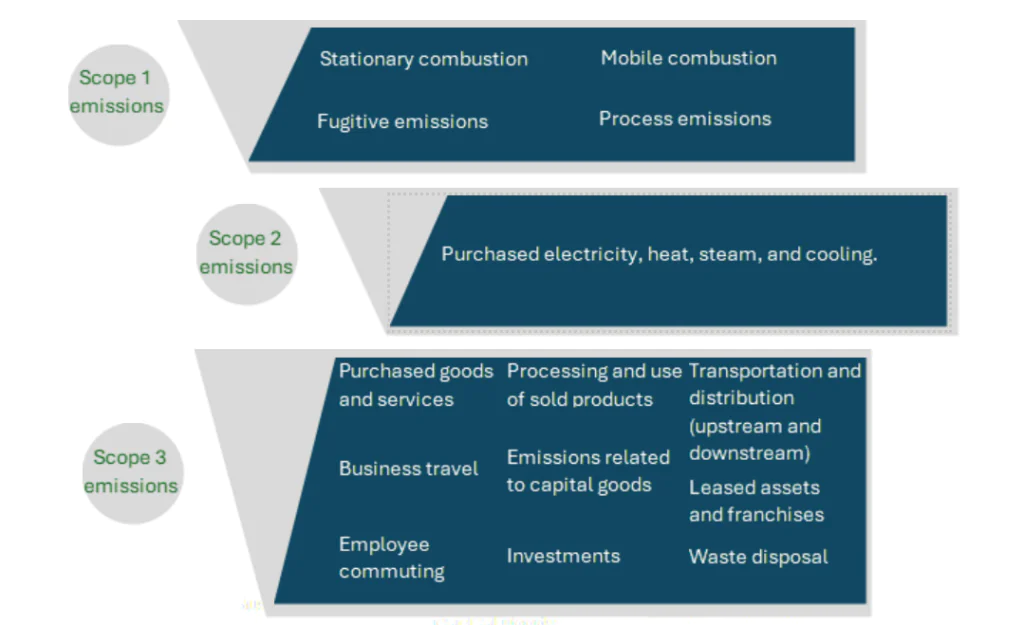

What are the sources of Scope 1, 2 and 3?

Scope 3 emissions and GHG Protocols (US and EU)

The categorization of emissions into different Scopes is a defining feature of the GHG protocol. Governments across the globe are universally adopting the categorization/standards related to emissions, as climate change is a universal problem and the issues related to climate change span national borders.

The development of the standards consisted of a broad and all-inclusive multi-stakeholder process, wherein the GHG accounting and reporting standards were developed in conjunction with businesses, government agencies, NGOs, and academic institutions worldwide. In 2008, World Resources Institute (WRI) and World Business Council for Sustainable Development (WBCSD) launched a three-year process to develop these new standards. Strategic direction for the process was provided by a 25-member steering committee of experts. The first drafts of the standards were developed in 2009 by technical working groups consisting of over 207 members from various industries, government agencies, academic institutions, and non-profit organizations across the globe. Also, in 2010, 60 companies from a variety of industries road-tested the standards and provided feedback regarding their practicality and usability. The organizations participating in the testing included companies such as 3M, DuPont, PepsiCo, Pfizer, BASF, and AkzoNobel, among others. In addition, more than 2,300 participants formed a stakeholder advisory group that provided feedback on each draft of the standards.

Situation in the UK

Today, governments and environmental organizations, such as the EPA in the US, are aware of the relevance and importance of Scope 3 emissions and are trying to help businesses assess, measure, and minimize such emissions.

Also, the SEC released a final draft of its climate disclosure rule on March 6, 2024. This rule encompasses Scope 3 emissions, and the final draft will require many companies listed in the United States to provide disclosures regarding GHGs and specify expected impact of climate-related risks.

Situation in the US

In the European Union (EU), the Carbon Border Adjustment Mechanism (CBAM) is a tariff on carbon-intensive products imported by members of the region. CBAM considers both direct and indirect emissions (including Scope 1, Scope 2, and some Scope 3). The CBAM has become applicable to all in-scope products from October 2023, ahead of its full rollout in 2026. The tariff currently covers industries such as electricity, hydrogen, cement, fertilisers, aluminum and iron and steel. More industrial sectors such as oil refining, upstream (fuel production), glass and ceramics, acids and organic chemicals, metals, pulp and paper, maritime, aviation, and lime will be added in 2030.

Benefits of assessing and measuring Scope 3 emissions for companies

- Help businesses assess emission identify hotspots across value chains and enable prioritization of reduction strategies

- Assist organizations in categorizing suppliers as leaders and laggards in terms of their sustainability performance

- Enable informed decision making across procurement, product development, and logistics teams regarding interventions that can deliver the most significant emission reductions

- Encourage innovations to create more sustainable and energy-efficient products

- Help advance strategies to create genuine, quantifiable, and visible change regarding decarbonization thus contributing toward achieving Net Zero targets

- Allow organizations to positively engage with employees to reduce emissions from business travel and employee commuting

- Assist in prioritizing de-carbonisation efforts and identifying areas where the biggest difference can be made

- Help businesses collaborate with suppliers to reduce emissions and demonstrate community level benefits of supply chain decarbonisation

- Assist organizations in communicating a comprehensive footprint and progress with stakeholders, such as constituents and communities

| Procurement centric | Focus on building capability |

| Organizations are adopting measures that can help them embed decarbonization into procurement processes, such as mandatory carbon reporting and carbon reduction requirements in tender proposals. Also, measures such as inclusion of carbon reduction clauses in performance management contracts and specification of penalties, such as termination of contracts of suppliers that fail to meet criteria, are being increasingly adopted. | This involves sharing learnings and leading practices related to carbon-reduction efforts being adopted by different organizations via supplier forums and workshops. Also, training and upskilling of suppliers in key areas related to decarbonization along with peer benchmarking to let suppliers know how they compare to their competitors. |

| Rewards and incentives | Enforcement |

| Organizations are providing financial incentives for achieving decarbonization goals, such as financially rewarding a supplier when it meets an emissions target. Also, organizations are looking to invest in promoting long-term initiatives such as power purchase agreements or carbon inset projects of suppliers as well as paying premium prices for low-carbon products and providing preferential payment terms for fulfilment of carbon-reduction targets. | This involves adopting measures such as levying financial penalties for failure to meet decarbonization targets. Adoption of such measures can shift accountability to suppliers. Also, direct financial penalties can be agreed upon and levied for scenarios such as failing to meet net zero targets. |

| Signify N.V. | IBM |

| Formerly known as Philips Lighting N.V., a Dutch multinational lighting corporation, has announced that it halved its GHG emissions since 2019 and cut its emissions by 22% in 2023 compared to 2022. The company also stated that it has included Scope 3 emissions to its environmental accounting this year. It stated that though the Paris Agreement is targeting a 30% reduction in Scope 3 emissions by 2030 compared to a 2015 baseline to achieve a 1.5°Celsius reduction, the company had already achieved a 61% reduction, thereby surpassing the target. | An American technology company, disclosed recently that it reports Scope 3 emissions in five of the fifteen categories defined by the GHG Protocol’s Corporate Value Chain Emissions Accounting and Reporting standard. IBM considers Scope 3 emissions related to the purchased goods and services category for its calculations, namely, emissions associated with electricity consumed in third-party operated spaces leased out by IBM (co-location data centers). The company is setting goals in alignment with scientific recommendations of the Intergovernmental Panel on Climate Change that aims to limit climate change to 1.5°Celsius above pre-industrial levels. |

Between January and June 2010, 34 companies had implemented the GHG Protocol Scope 3 Standard in their organizations in a bid to provide WRI and WBCSD feedback on the practicality of the standards. In May 2010, the companies participated in an in-person workshop in Washington DC and submitted their inventory reports and detailed written feedback by mid-2010.

Companies participating in the road-testing exercise pertaining to the Scope 3 Accounting and Reporting Standards found that it was possible to complete a Scope 3 inventory and many of these companies felt that it was practical to complete an inventory annually.

Given below are the names of some companies that participated in this exercise.

| 3M | Mitsubishi Chemical Corporation |

| Abengoa | National Grid |

| Acer Inc. | New Belgium Brewing |

| Airbus S.A.S | Ocean Spray Cranberries |

| AkzoNobel | PE International |

| Amcor | Pfizer |

| Autodesk Inc. | Pinchin Environmental Ltd. |

| Baoshan Iron & Steel Co. Ltd. | PricewaterhouseCoopers |

| BASF SE | Procter & Gamble Eurocor |

| Coca-Cola Erfrischungsgetränke AG | Public Service Enterprise Group Inc. |

| Danisco A/S | SAP AG |

| Deutsche Post DHL | SC Johnson |

| Deutsche Telekom AG | Shanghai Zidan Food Packaging and Printing Co., Ltd. |

| Ford Motor Company | Shell International Petroleum Company Ltd. |

| IKEA | Siemens AG |

| Italcementi Group | Suzano Pulp and Paper |

| Kraft Foods | Swire Beverages |

| Lenovo | Veolia Water |

| Levi Strauss & Co. | Webcor Builders |

The emissions are categorized into Scope 1, 2, and 3; however, this classification and related standards are not a part of any act or regulation; however, they are aligned with existing environmental regulations and, thus, have become generally accepted norms. Companies and organizations are not bound to accept them but most of them are voluntarily adopting these norms because it helps them manage their GHG emissions better if they can classify them based on their source.

Today, governments and companies across the globe are cognizant of this classification and coming up with plans for decarbonization based on this categorization, and it is expected to become a universally recognized and accepted norm in the near future.